TL:DR summary

- Poland’s National e-Invoice System, KSeF (Krajowy System e-Faktur), is now in its mandatory phase for B2B e-invoicing

- From 1 February 2026, large taxpayers must issue B2B e-invoices via KSeF, with the mandate expanding to all remaining businesses from 1 April 2026

- The Poland KSeF mandate starts with large taxpayers and then expands to most businesses in April

- B2B invoices must use FA(3) (Poland’s EN 16931-based XML schema), and B2G e-invoicing can still use Peppol BIS Billing 3.0 via the PEF platform

- To stay compliant, businesses need to be able to send and receive structured invoices in the required schema and manage authentication, error handling and business continuity

E-invoicing in Poland: an overview

Poland’s journey to mandatory e-invoicing has been gradual.

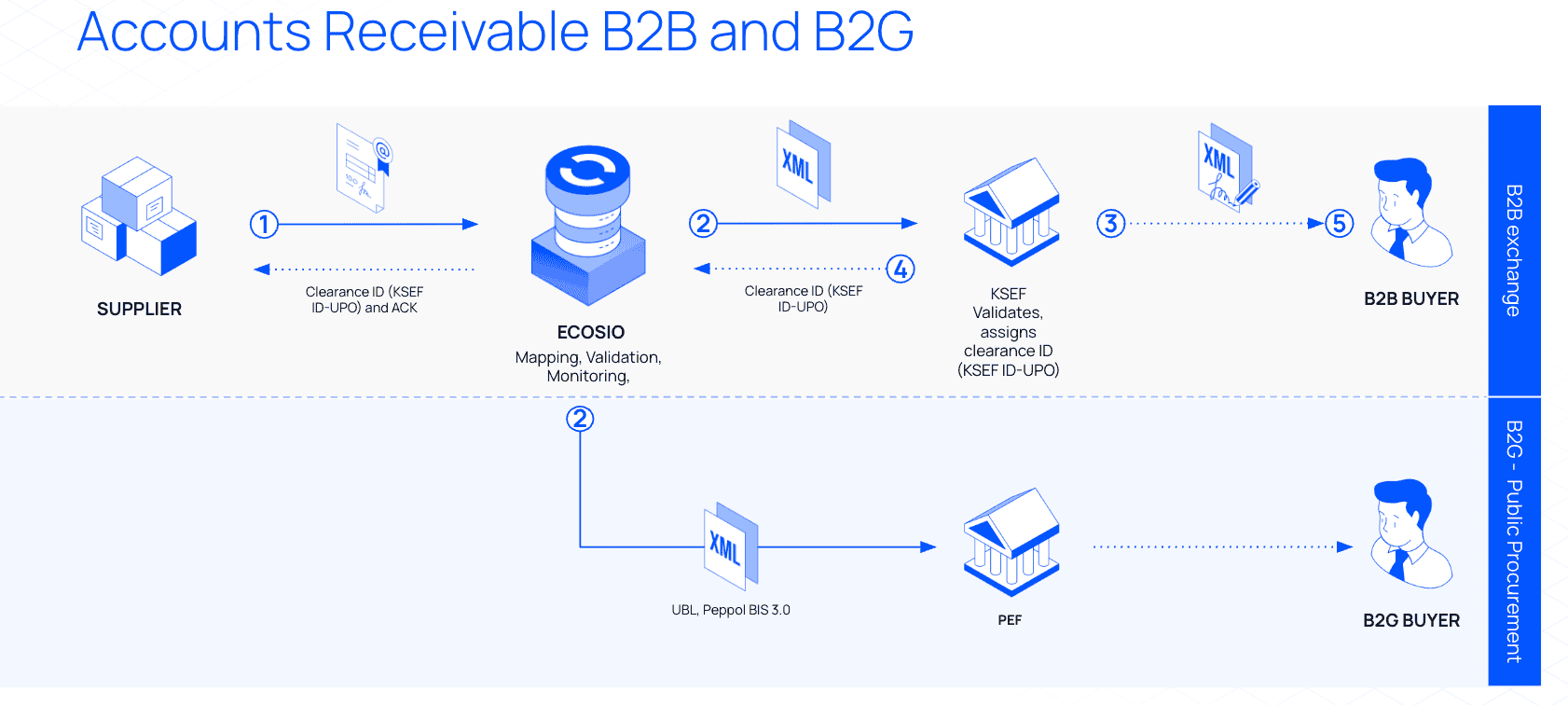

From 2019 until now, B2G e-invoicing has been supported via PEF (Platforma Elektronicznego Fakturowania). However, KSeF (Krajowy System e-Faktur) was implemented as Poland’s e-invoicing system to validate and clear structured invoices before they become legally effective. KSeF has been available for voluntary use since 2022. With the implementation law signed in August 2025, Poland has moved into a phased mandatory rollout.

Instead of exchanging invoices directly in whatever format two businesses agree on, suppliers submit structured invoice data to KSeF, which validates the invoice and assigns a unique reference (often referred to as the KSeF number) before the buyer retrieves it.

This is the core of the Poland KSeF mandate and it is why businesses need a reliable process for both submission and retrieval.

This approach aims to standardise invoicing, reduce fraud and give the tax authority better visibility of VAT-relevant transactions.

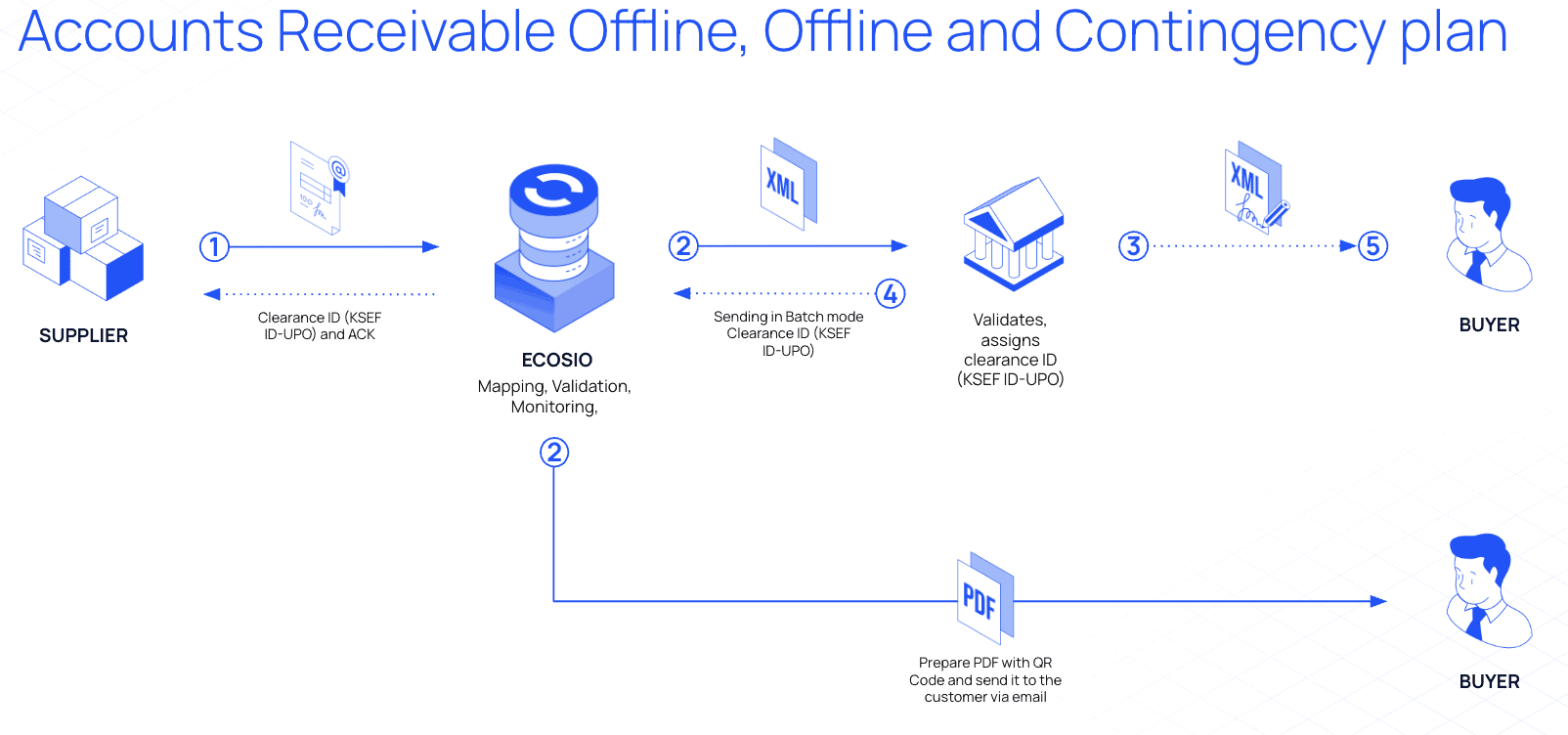

In rare outage scenarios, Poland supports an offline contingency procedure. This allows invoices to be issued locally and submitted to KSeF once the platform is available again, which is why it’s worth defining business continuity ownership in advance.

If your organisation sells into Poland, buys from Polish suppliers, or has an established entity that invoices customers in Poland, it’s important to understand when the mandate applies and what it means for your invoicing and ERP system processes.

For an up-to-date compliance view, you can also check ecosio’s Poland country information page: Poland e-invoicing compliance overview.

Poland’s e-invoicing journey: a timeline

Poland has been evolving towards mandatory structured e-invoicing for several years, with the most important milestones now landing in 2026:

- 1 February 2026: Mandatory B2B e-invoicing via KSeF starts for large taxpayers with annual revenue exceeding PLN 200 million.

- 1 February 2026: B2G invoicing can be handled via KSeF or PEF (Platforma Elektronicznego Fakturowania), which uses the Peppol framework.

- 1 April 2026: Mandatory B2B e-invoicing expands to all remaining taxpayers.

- 1 January 2027: Mandatory e-invoicing requirements extend to the smallest taxpayers (where applicable under the final scope and exemptions).

How regulations may affect you

Mandatory KSeF changes both the format and the process of invoicing.

Even if your finance team already sends PDFs today, B2B e-invoicing Poland requires structured invoice data to be submitted through the government platform for clearance.

E-invoicing is also part of a broader push towards digital tax control in Poland. Many organisations already know Poland for its SAF-T (JPK) reporting requirements, which reinforces why it is worth treating KSeF as a strategic compliance capability rather than a one-off IT project. If you’re tracking multiple mandates across Europe, it is worth treating Poland as a priority rollout.

For many businesses, the biggest changes are practical rather than theoretical:

- You need to support structured invoice generation and mapping into the Polish schema and validation rules. At a high level, most businesses need to plan for two parallel requirements:

- B2B: structured invoices cleared through KSeF (FA(3) XML)

- B2G: structured invoices through PEF, using the Peppol framework (where relevant for your customer base)

- Your invoicing process needs status handling, so you can confirm which invoices were accepted and which were rejected.

- You need buyer and supplier readiness. Even if your organisation is not yet required to issue invoices through KSeF on day one, VAT-registered entities still need to be ready to receive and process invoices coming through the platform as the rollout begins:

- If you issue invoices, your buyers will receive invoices via KSeF.

- If you are preparing for B2B e-invoicing Poland, make sure your AR and AP teams agree on who owns rejections, retries, and customer communication.

- If you receive invoices, you must be able to retrieve supplier invoices from KSeF and feed them into AP processes.

- You need business continuity planning for platform outages.

- KSeF supports offline issuance scenarios, but businesses still need a controlled way to issue invoices and submit them when services are restored.

If you want a quick refresher on core concepts, see ecosio’s overview: E-invoicing basics and key terms.

What are the penalties for non-compliance?

Non-compliance can create serious financial and operational risk. While enforcement guidance can change, public summaries indicate the following:

- During 2026: Poland has announced a grace period, meaning no financial penalties are expected to be imposed for KSeF non-compliance until 1 January 2027.

- From 1 January 2027: financial penalties can apply. Public summaries indicate fines up to 100% of the VAT amount on the invoice if an invoice is not issued via KSeF when required (and additional consequences may apply for repeated non-compliance).

Even with the grace period, when a business cannot issue compliant invoices, it may not be able to bill customers on time, which can impact cash flow.

Rejected invoices can also create downstream issues for customers and suppliers, including disputes and payment delays.

To dig deeper into Poland’s mandate, a good place to start is the official authority KSeF information site, which contains legal and technical resources: KSeF portal.

How to achieve compliance

KSeF compliance is easiest when you treat it as a cross-functional rollout.

These steps also help you meet KSeF requirements Poland-based teams typically need to align across finance, tax, and IT.

A practical approach looks like this:

Confirm scope for your business

- Clarify whether your invoice flows fall under the Poland e-invoicing system scope for mandatory clearance and retrieval.

- Identify which Polish entities, VAT registrations and invoice flows fall into the mandate.

- Separate B2B, B2G and cross-border scenarios.

Align internal stakeholders early

- Finance and tax define compliance requirements and exception handling.

- IT confirms ERP system integration approach and delivery timelines.

- Sales operations and customer support prepare for buyer questions about invoice delivery.

Choose your integration model

- Direct integration to KSeF can work for single country use cases, but often adds long-term maintenance overhead.

- A managed provider can reduce the burden of schema updates, validation changes and ongoing monitoring.

Prepare authentication and access controls

- Your team needs a secure way to authenticate to KSeF (e.g. using the supported credential methods) and manage authorisations.

Use the available testing period to validate your end-to-end integration

- Validate invoice data quality, FA(3) mapping, authentication, and rejection handling, so you are not debugging critical flows close to the mandatory dates.

- Confirm acceptance and rejection paths.

- Verify how you capture and store the KSeF reference returned by the platform.

Plan for go-live and business continuity

- Define operational ownership for exceptions.

- Plan what happens if KSeF is temporarily unavailable, including offline issuance and later submission processes.

Your two compliance options compared

Option one: build and manage in-house

- Best suited when Poland is your only mandatory structured e-invoicing requirement and your internal team can own ongoing changes.

- You still need to maintain schemas, API changes, validation logic and monitoring over time.

Option two: outsource to a fully managed provider

- Best suited when you operate across multiple jurisdictions or want a lower operational burden.

- You gain a single integration point and a partner to handle country updates, monitoring, and exception management.

How ecosio can help

ecosio’s Global E-invoicing Compliance helps you connect once and comply with many country mandates, including Poland’s KSeF.

With ecosio, you can:

- Set up your connection to Poland’s KSeF quickly using ecosio’s self-service country connector in the ecosio Monitor, with guided steps for credentials, authentication, and error handling (For more info, read our article on Self-service connectors)

- Automate compliant invoice submission for accounts receivable and retrieve invoices for accounts payable.

- Validate and map invoice data into the required Polish format and handle responses and statuses end to end.

- Poland’s framework may evolve, so monitoring government guidance and aligning with your tax and legal teams is crucial. A managed compliance platform tracks mandate changes globally and ensures always-on compliance, letting you focus on your business’ core priorities.

- Reduce internal firefighting with clear monitoring, exception handling, and support for outage scenarios.

If you’d like to discuss your Poland rollout, the simplest next step is to talk through your invoicing flows and timeline with our team: get in touch with ecosio.

For a deeper technical overview, you can also watch ecosio’s webinar: E-invoicing in Poland: What You Need to Know.

The April go-live date is close and the operational impact is significant, especially for high invoice volumes or complex billing models. Reach out to ecosio so we can address your particular situation.

Ready for Poland’s KSeF E-invoicing?

ecosio’s core competency is smooth ERP integration, providing the infrastructure to meet Poland’s specific e-invoicing demands, including the National e-Invoicing System (KSeF). To ensure your company remains ahead of the curve and in full electronic compliance, connect with us for a consultation.

Operating in other European countries? We got you covered. Check out our existing blogs on Italy (link), Belgium (link), Germany (link), and beyond, to stay up to date with the latest advancements in e-invoicing.

If you’d like to explore what compliant KSeF set-up could look like for your specific invoice flows, you can get in touch with ecosio.

Frequently asked questions

Is e-invoicing mandatory in Poland in 2026?

Yes. Poland is rolling out mandatory B2B e-invoicing through KSeF in phases in 2026, starting with large taxpayers on 1 February 2026 and expanding to all remaining taxpayers on 1 April 2026.

What is KSeF?

KSeF (Krajowy System e-Faktur) is Poland’s central platform for issuing and receiving structured invoices. It is the Polish e-invoicing system used to validate invoices and make them available to recipients.

Invoices are validated within the system and assigned a unique reference number that supports traceability.

What invoice format is required?

For invoices issued through KSeF, Poland uses a specific structured XML schema.

From 1 February 2026, the FA(3) XML schema is the mandated structured format for KSeF flows.

Does Poland require an electronic signature on e-invoices?

Poland’s KSeF approach focuses on structured submission and platform validation.

Electronic signature requirements can depend on your scenario and internal controls, so it is best to confirm with your tax and legal team.

What happens if KSeF is unavailable? Can we still issue invoices in Poland?

Yes. Poland has created a contingent scenario for rare outage situations, known as offline mode. With an offline certificate (a locally stored signing certificate), you can continue issuing invoices while KSeF is unavailable by signing them locally, storing them with a timestamp and signature, and marking them as issued in offline mode.

Once KSeF becomes available again, the signed invoice must be submitted to KSeF so it can be validated and assigned a KSeF ID.

The offline certificate is optional but strongly recommended and supported by ecosio. Without it, you typically need to wait until KSeF is back online, which can delay invoicing and increase operational risk.

What about B2G invoicing in Poland?

From 1 February 2026, businesses have been able to use either PEF or KSeF for B2G invoicing.