Germany is introducing mandatory e-invoicing for domestic B2B transactions. In practice, this means moving from “visual invoices” (PDFs and paper) to structured, machine-readable invoices that your systems (e.g. ERP) can process automatically.

The legal changes stem from Germany’s Growth Opportunities Act (Wachstumschancengesetz) that introduced e-invoicing requirements in Germany with the goal of standardising invoice data, improving the VAT gap (the largest in the EU in absolute monetary terms), and preparing the country for future EU-wide initiatives like VAT in the Digital Age (ViDA).

Looking to stay up-to-date with German e-invoicing regulations?

Our Germany e-invoicing page is constantly updated to reflect the latest requirements

TL;DR summary

- Since 1 January 2025 businesses have been required to be able to receive and process structured e-invoices for domestic B2B

- PDF and paper invoices are no longer acceptable, as compliant e-invoicing requires machine-readable, structured data

- Compliance is based on EN 16931, with common formats including XRechnung, UBL, CII, and ZUGFeRD (2.1+)

- Mandatory issuing starts in January 2027 for larger businesses, and expands to all businesses in January 2028

- There is no central clearance platform, so the recipient’s validation rules and buyer-specific requirements often decide whether invoices are accepted, even if they are compliant

- E-invoices must be kept in their original electronic format for up to 8 years

How to prepare (practical priorities):

- Make AP ready for structured invoices: choose supported formats, validate, map into your ERP system, and define exception handling

- Prepare AR early: align required reference fields with key customers (e.g. PO numbers and routing codes) to reduce rejections and late payments

- Put governance and monitoring in place: clean master data, set ownership for invoice data fields, and track delivery and processing outcomes

Germany’s e-invoicing journey: a timeline

Germany’s B2B rollout is phased, so many businesses will be receiving structured e-invoices earlier than they are required to issue them.

| Milestone | What it means in practice |

|---|---|

| 1 January 2025 | All businesses must be able to receive structured e-invoices for domestic B2B transactions. |

| Until 31 December 2026 | Voluntary outbound e-invoicing for domestic B2B transactions |

| 1 January 2027 | Businesses above a turnover threshold (commonly referenced as over 800,000 EUR) must issue structured e-invoices. |

| 1 January 2028 | All businesses must issue structured e-invoices for domestic B2B transactions. |

How is Germany’s mandate different?

Germany is taking a decentralised, post-audit approach to B2B e-invoicing. This is a key difference compared to “clearance” models used in some other European countries like France and Poland.

In clearance countries (e.g. France and Poland):

- Invoices are typically routed through a government-controlled platform

- The invoice often needs to be validated, cleared, or reported before it is considered properly issued

- Rejections and status updates are closely tied to the platform workflow

In Germany’s decentralised post-audit model:

- There is no central B2B platform that invoices must pass through

- Buyers and suppliers exchange invoices directly via agreed channels such as Peppol, email, EDI, or portals

- Tax authorities do not receive a real-time copy by default, but they can request invoices during an audit

Why this matters operationally

Because there is no government “gatekeeper”, validation at the recipient side becomes the practical enforcement mechanism. If your invoice data fails EN 16931 rules, or it does not meet buyer-specific processing requirements, you can still end up with rejected invoices, delayed payments, and manual rework even when the invoice is legally valid.

How regulations may affect you

The impact depends on where the biggest invoicing workload sits today.

- If you receive many supplier invoices (AP), your first priority is receiving readiness. From 1 January 2025, you need a process that can accept structured files, validate them, and feed them into your ERP system.

- If you send many customer invoices (AR), you have a transition window, but it is worth standardising early. You will need a repeatable way to generate EN 16931-compliant invoices, agree an exchange method with customers, and manage exceptions.

- If you operate across multiple entities or ERP systems, e-invoicing typically becomes a coordination challenge. Standardising formats and validation upfront reduces rework later.

Who needs to comply (and what is in scope)?

For B2B, the mandate focuses on domestic transactions where both supplier and buyer are established in Germany and the supply is within scope of German VAT rules.

Typically in scope

- Domestic B2B sales of goods and services between German-established businesses

- VAT-relevant invoices that must meet standard invoicing requirements

Commonly out-of-scope/exempted:

- B2C transactions

- Cross-border transactions (incoming or outgoing)

- Small-amount invoices (e.g. under 250 EUR) and other specific exemptions

There are separate rules and platforms for B2G (business-to-government) invoicing. Germany has required B2G e-invoices (XRechnung) since 2020, often via state or federal portals. See more about Germany’s B2G mandate here

What are the penalties for non-compliance?

The biggest operational risk is rejected invoices, delayed payments, and manual rework that scales with invoice volume.

For regulated penalties, Germany’s fiscal code includes a framework for fines in certain cases of non-compliance. Even when direct penalties are not applied, non-compliant invoicing can still create downstream impacts, such as disputes, slower cash collection, and audit exposure.

How to achieve compliance

A practical approach is to treat compliance as a short sequence of measurable steps.

- Map your current invoice flows (inbound and outbound) and identify where PDFs, paper, or legacy EDI formats are still dominant

- Confirm scope (domestic B2B, exemptions, cross-border) and align stakeholders in your tax, finance and IT teams on what must change first

- Choose your target format(s) (EN 16931 compliant), and ensure you can receive and generate the formats your trading partners will use

- Implement validation and exception handling to reduce rejected invoices and manual corrections

- Establish data governance to define ownership of invoice master data internally, therefore reducing rejection and exception queues

- Agree transmission methods with key trading partners (email, Peppol, EDI, or direct integration), and set up monitoring for delivery and receipt

- Set up compliant archiving that keeps the original electronic file and supports audit access

- Pilot and iterate with a subset of suppliers and customers before scaling

Compliance vs commercial acceptance

Even if an invoice is fully compliant with German VAT rules and EN 16931, it can still be rejected by the buyer’s systems.

That is because many buyers run straight-through processing and automated matching. If a legally valid e-invoice is missing a purchase order number, routing code, cost centre, internal buyer identifier, or other partner-specific fields, it may be pushed into an exception queue or rejected entirely. In practice, this can lead to:

- Silent delivery failures

- Delayed payments

- Extra manual work on both sides

To avoid this, treat e-invoicing as a joint process with your trading partners, not just a file format change. Strong data governance, clean master data, and clear partner alignment are often the difference between “compliant” and “paid on time”.

What formats are accepted in Germany?

Germany requires e-invoices to be compliant with EN 16931 (the European standard for e-invoice data). In practice, this includes several syntaxes that are widely used in Germany and across the EU:

- XRechnung (commonly used for B2G, also accepted in B2B)

- UBL 2.1

- CII (Cross Industry Invoice)

- ZUGFeRD (hybrid PDF/A-3 with embedded XML, for the correct EN 16931 profiles)

- If the PDF and embedded XML differ, the XML is legally authoritative.

A key point is that “XML” alone is not a compliance indicator. The file needs to follow an accepted EN 16931 implementation.

Is there a central platform for B2B e-invoices in Germany?

No. Germany’s current approach for B2B is decentralised. Businesses exchange e-invoices directly, using channels they agree on, such as:

- Email (structured attachment)

- EDI

- Networks like Peppol

- Direct ERP or API integrations

This differs from clearance models where invoices must be routed through a government platform in real time.

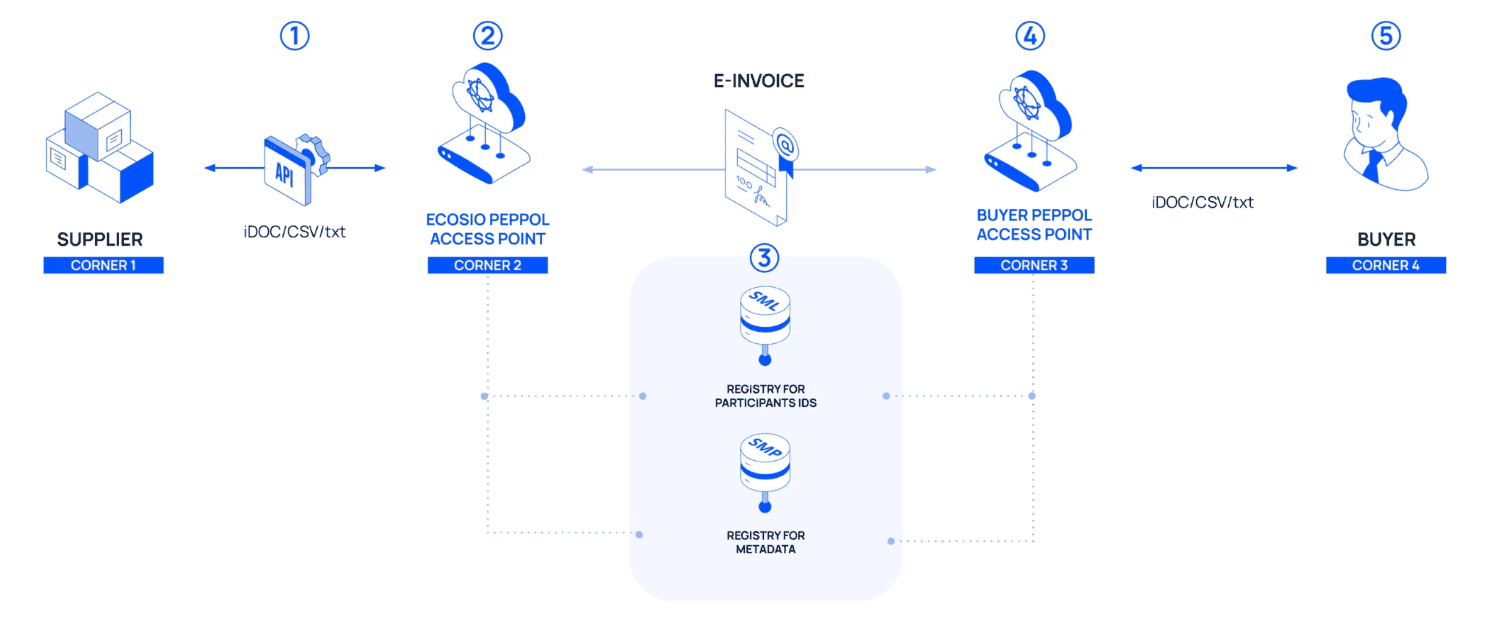

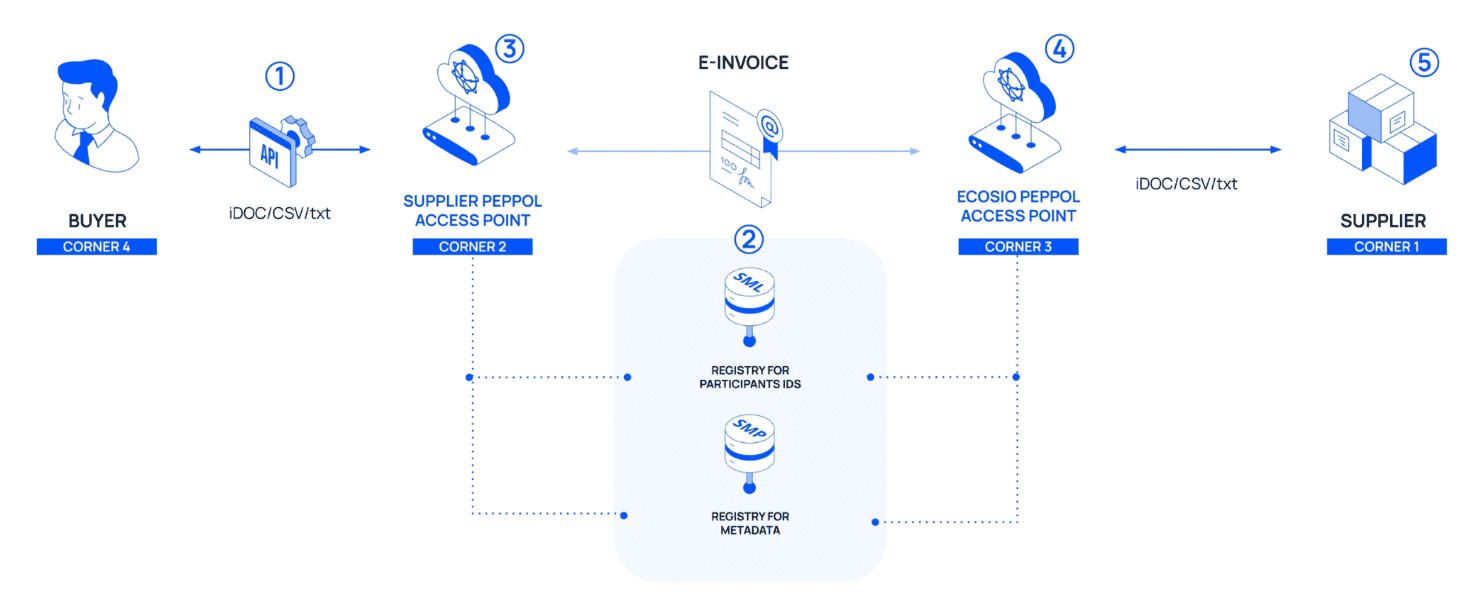

Peppol in Germany (B2B): what it means in practice

Peppol is not mandatory for Germany’s B2B e-invoicing mandate, but it is a widely used way to exchange structured, EN 16931-compliant invoices in a consistent, scalable way. It can support both inbound and outbound flows, provided you still meet the format and data requirements your trading partners expect.

Peppol for AP (receiving supplier invoices)

For accounts payable (AP), Peppol can help you receive structured e-invoices in a predictable way, with standardised addressing and delivery. However, “received” does not automatically mean “processable”:

- You still need to validate the invoice content against EN 16931 and your internal business rules

- You still need mapping into your ERP system and a clear process for exceptions

- You should align required reference fields with key suppliers (e.g. purchase order number, cost centre, routing details), so invoices do not fail automated matching

Peppol for AR (sending customer invoices)

For accounts receivable (AR), Peppol can reduce the complexity of onboarding many customers because you can use a standard network for delivery instead of maintaining multiple point-to-point connections.

To avoid payment delays:

- Confirm which EN 16931 syntax your customer expects (e.g. UBL profile) and test early

- Agree the “must-have” data fields for your customer’s straight-through processing, not just the minimum legal fields

- Set up monitoring and acknowledgements where available so you know when delivery or processing fails

Archiving and retention: how long do you need to store e-invoices?

E-invoices must be archived in their original electronic format, ensuring that authenticity and integrity are preserved. As a practical best practice, invoices must remain readable, searchable, and exportable for the duration of their retention to ensure audit readiness.

Retention period updated to 8 Years:

While many older summaries and general EU guidelines reference a 10-year archiving requirement, Germany recently reduced this. Under the Fourth Bureaucracy Relief Act (Bürokratieentlastungsgesetz IV), effective1 January 2025 the mandatory retention period for invoices and booking vouchers under § 147 AO and § 14b UStG has been shortened from 10 years to 8 years. (Note: This 8-year rule applies to all invoices whose original 10-year period had not yet expired by 31 December 2024).

GoBD and the Retention of Intermediary Formats:

Because Germany requires archiving the “original” electronic format, special attention must be paid to how the invoice is generated and processed under the German GoBD (Principles for the Proper Keeping and Storage of Books, Records and Documents in Electronic Form).

If an invoice undergoes a mapping or conversion process (e.g. transforming an ERP-generated data file into the final compliant XML or ZUGFeRD format), intermediary artifacts and source files may also need to be retained and linked to the final invoice. The only way to avoid archiving these intermediate formats is if the mapping/conversion approach qualifies as a fully compliant transformation under the GoBD. This means the transformation must be strictly deterministic, preserve full integrity, and result in absolutely no semantic changes to the data. Until a solution’s conversion process is formally assessed and validated against these GoBD standards, it is safest to assume that intermediate artifacts should be archived alongside the final outbound invoice.

How ecosio can help

Getting compliant should not require a patchwork of one-off integrations and constant firefighting.

With ecosio’s Global E-invoicing Compliance solution, compliance with Germany’s e-invoicing regulations becomes easy. You benefit from…

- Format compliance for EN 16931 syntaxes (including XRechnung, UBL, CII, and ZUGFeRD)

- Validation and monitoring to reduce rejections and manual rework

- Flexible exchange options (e.g. Peppol and email), depending on what trading partners can support

- Support for both inbound (AP) and outbound (AR) flows

Conclusion

Germany’s B2B e-invoicing mandate represents a major shift for tax, finance and IT teams, but the phased timeline gives you time to build the right foundations. The safest approach is to treat 2026 as the year to strengthen receiving, validation, and archiving, then use the transition window to standardise issuing and partner onboarding ahead of 2027 and 2028.

If you want to keep tracking key deadlines, scope, and accepted formats, see our Germany e-invoicing country page.

Ready to reduce compliance risk and avoid rejected invoices? Get in touch to see how our Global E-invoicing Compliance solution can support your AP and AR processes.

Frequently asked questions

Is a PDF invoice compliant with Germany’s B2B mandate?

A standard PDF is not considered a structured e-invoice. For in-scope B2B transactions, the compliant invoice must be machine-readable and EN 16931-aligned.

Is Peppol mandatory in Germany?

Peppol is accepted and widely recommended, but it is not the only option. Businesses can agree to other compliant transmission methods as long as the invoice stays structured.

What if a business mainly sells to consumers?

Even if most sales are B2C, businesses still need to be ready to receive structured e-invoices from suppliers for B2B purchases.

Do foreign businesses need to comply?

The B2B mandate focuses on domestic transactions between parties established in Germany. Requirements for non-resident setups depend on whether there is a local establishment and the specific transaction.